The Calm Before the Crash

Why Low Risk Readings Are the Warning Sign

Every financial crisis is preceded by a period of unusual calm. The fear gauge reads low, the models flash green, positions net cleanly. Then the floor disappears.

This is not a new observation. That stability breeds instability is one of the more durable findings in financial economics — Minsky’s financial instability hypothesis made it decades ago, and the modern theory of endogenous risk (Danielsson and Shin, 2003) formalised the mechanism: risk models used simultaneously by many institutions generate the very fragility they fail to measure. Measured risk understates true risk precisely because the measurement is endogenous to the system being measured. None of that is my claim, and the reader should hold me to a narrower one.

What I want to add is a change in how we categorise the failure — and, from it, a suggestion about what to build. Not that models underestimate risk in calm periods, which is established, but that in those periods the standard metrics have often stopped being valid at all — they have quietly left the regime in which they mean anything. That is a different kind of failure than underestimation, and it implies a different kind of instrument.

The Mismeasurement

Start with the number most commonly cited as evidence that the system is out of control: the global derivatives market, roughly $846 trillion in notional value (BIS OTC statistics, end-June 2025), about eight times world GDP. The figure is real; the inference usually drawn from it is not.

Notional value records the face amount of all outstanding contracts, most of which offset one another. Netted to gross market value, true economic exposure falls to about $21.8 trillion — roughly 97 per cent cancels. The size of the aggregate stack is therefore a poor proxy for systemic risk. This displaces rather than resolves the question: if scale is not the operative variable, what is?

The Mechanism

Risk models embed assumptions — about volatility, correlation, and the shape of return distributions. In quiet periods those assumptions decay away from reality without triggering revision, because no event has yet forced a repricing. Volatility looks low; correlation looks manageable; tails look thin. The models report a benign state, and the benign reading is the hazard: low measured risk often indicates that the distance between what the model assumes and what the world is doing has grown to its widest point. A crisis is the repricing of that accumulated divergence, all at once.

So far this is the endogenous-risk account in plain language. The turn I want to make is on the nature of the gap.

Two Kinds of Model Failure

There is a standard way to describe what goes wrong: the models underestimate risk. On this view the metric is inaccurate — it returns a number that is too low, and the fix is a better-calibrated number. The correction lives inside the model’s own frame; you re-tune the parameters and carry on.

There is a second, sharper description. In certain regimes the metric is not merely inaccurate but inapplicable — it has left the conditions under which it carries any meaning. This is, in one sense, an old distinction in new clothes: econometrics separates estimation error (the right model, wrong parameters) from specification error (the wrong model), and statistical learning separates estimation from approximation error. What I am claiming is not the distinction but its transfer — that systemic-risk measurement fails, in calm periods, on the specification side far more often than the vocabulary of “underestimation” admits, and that this changes what an instrument should do.

The transfer is not clean, and I should say where it strains. The drift described above is continuous: assumptions decay by degrees. A strict difference in kind therefore cannot live in the magnitude of the gap. It lives, if anywhere, at the boundary between recalibrating within a model class and moving to a different class — and that boundary is drawn by the analyst, not handed down by the world. Whether replacing a fixed-correlation value-at-risk model with a regime-switching one counts as recalibration or as changing the frame is partly a modelling convention. So “inadmissible” is boundary-relative in a way “underestimated” is not, and the reframing has to carry that cost rather than hide it.

Even granting the cost, the second failure arrives in at least two forms, and they are worth keeping apart. In the first, the metric’s validity conditions fail: a value-at-risk figure computed on stable correlations does not become a slightly-wrong number when correlations break — it becomes the consequent of a conditional whose antecedent is now false, a measurement reporting with full confidence from outside its domain. In the second, the metric stays internally valid but the question it answers has gone stale: it measures faithfully, and measures the wrong thing, because the regime has moved the operative risk elsewhere. Both are inadmissibility; neither is underestimation; and the distance between them is exactly what will make a general instrument hard to build.

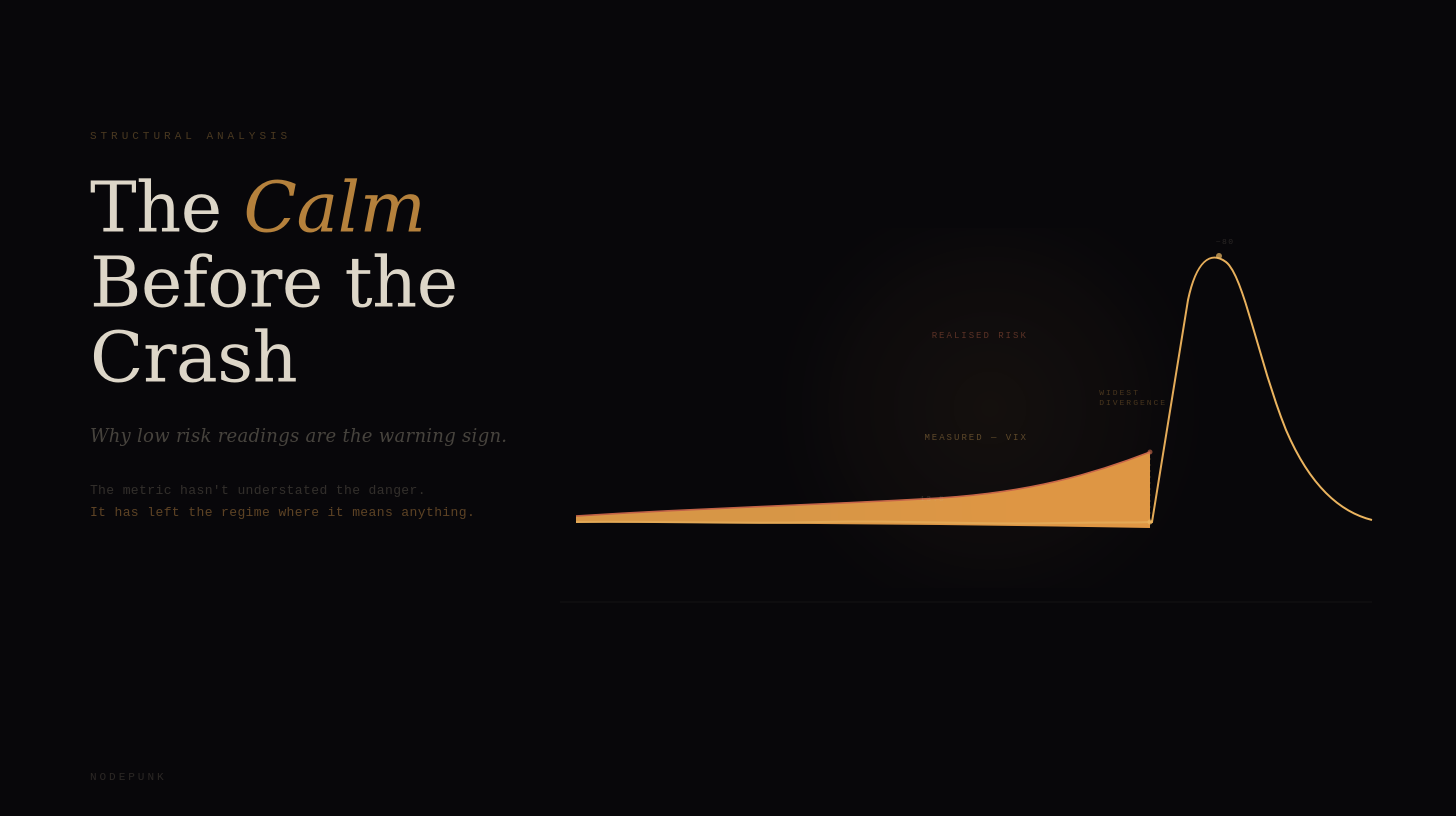

The VIX Before 2008

The VIX remained below 13.5 from September 2006 through February 2007, and averaged around 17 across 2007 — signalling tranquility straight into the worst financial crisis since the 1930s, before reaching roughly 80 in late 2008.

The index did not malfunction. It measured implied near-term equity volatility — how nervous participants were about the next thirty days — accurately. What it could not measure was the degree to which the underlying regime had left the conditions under which that measurement meant anything. This is the second form of inadmissibility: the number was not too low. It was answering a question that had stopped being the relevant one.

Silicon Valley Bank, 2023

SVB is the clean, bounded case — and the instructive one, because nothing was hidden. A sharp rise in interest rates was a regime change. The bank kept its prior frame: bonds held to maturity, carried at amortised cost, hedges removed. By early 2023 the mark on that book was disclosed — unrealised losses of about $15.2 billion against roughly $16 billion of equity. The number existed; it was not concealed by any model going dark. What failed was the decision to treat the amortised-cost frame as the operative description of solvency after the rate shock had made the mark the operative fact. As with the VIX, the accounting measured faithfully and measured the wrong thing. When the market repriced the divergence, resolution took seventy-two hours. No exotic instrument, no outsized external shock — a frame kept past its regime was enough.

Toward an Instrument

If the failure is inadmissibility rather than underestimation, the natural response is to measure the gap itself — to monitor not the risk number but the distance between a model’s assumptions and realised conditions, and to read a widening distance as the instrument leaving its regime.

Here I must be careful, because the terrain is occupied. The idea that model-reality divergence carries predictive information is not open to claim. The excess bond premium of Gilchrist and Zakrajšek (2012) isolates the component of credit spreads not explained by measured default risk — a deviation-from-fundamentals term — and it rises ahead of recessions. Christoffersen’s (1998) independence criterion for value-at-risk backtesting is, in effect, a regime-departure detector already: exceptions that cluster rather than arrive independently signal that a model has stopped tracking the prevailing volatility and correlation regime, and Basel’s conditional-coverage tests institutionalise exactly that reading. Any honest treatment has to cite these; the observation is theirs.

The integration point is weaker than it first appears, too. I wanted to claim that the existing indicators track single deviations in isolation, where a composite has not been assembled — but the New York Fed’s Corporate Bond Market Distress Index (Boyarchenko et al., 2022) is precisely a “preponderance of metrics” composite, and it predicts distress. Integration as such is not open ground. What appears still unclaimed is narrower: the CMDI integrates within one market’s functioning; it does not compose tail-divergence, correlation-divergence and repricing-latency across domains into a single regime-validity index, and framing those as symptoms of one condition — a measurement leaving its admissible regime — is a reorganisation I have not seen made. That is the residue of the claim, and it is thin.

Two admissions keep it honest. First, the cases above do not share a mechanism: validity-conditions-fail is not question-goes-stale, so a single composite presumes a commensurability between heterogeneous gaps that I have asserted, not shown. The unity is at the level of diagnosis, and whether it survives being made quantitative is open. Second, and worse for the programme: any such instrument is itself a model with assumptions — detecting a correlation break still means estimating correlations over a window whose stationarity you have assumed — so it can leave its own regime by the same logic. The gap-measure does not dissolve the out-of-regime failure; it relocates it to the checker. The most it can honestly promise is to push the boundary of confident measurement outward, not to abolish the blind spot behind it.

So I offer these as claims to be tested, not results. Whether such a composite would beat the blunt incumbents — simple leverage ratios, which the literature has repeatedly found hard to outperform near crises — is an open empirical question, and the existing evidence does not obviously favour the more sophisticated measure. There is also a test the distinction itself must pass. If inadmissibility only ever shows up as false calm before a crisis, it is not cleanly separable from “risk underestimated at the dangerous tail,” and earns no independent keep; it earns its keep only if a metric can be shown out of regime while reading as falsely alarming rather than falsely safe — a case I have not yet produced. I would rather state these as questions I am prepared to lose than as findings I have not earned.

The Inversion

There is a structural inversion at the heart of conventional risk measurement: the most-watched metrics are most reassuring exactly when the underlying position is most precarious. Low volatility is read as safety when it may mean the models have not been tested recently and have drifted furthest from reality. Low correlation is read as diversification when it may reflect a calm that will vanish precisely when diversification is needed.

The aggregate debt stock — about $348 trillion globally, roughly three times world output (IIF Global Debt Monitor, Q4 2025) — is not the crisis. The $846 trillion in derivative notional is not the crisis. These set the scale through which a repricing would move, but they are not where the risk lives. The risk is in the gap between the map and the terrain, at the moment everyone is most confident the two are aligned — and, more precisely, in our not yet having a good instrument for noticing when the map has stopped being a map at all.

This is Minsky’s thesis, not mine: stability does not merely precede instability — it generates it, by allowing that gap to widen uncontested until the system can no longer hold both pictures at once.

References

Bank for International Settlements (2025). OTC derivatives statistics at end-June 2025. https://www.bis.org/publ/otc_hy2512.htm

Boyarchenko, N., et al. (2022). The Corporate Bond Market Distress Index. Federal Reserve Bank of New York, Staff Report No. 957. https://www.newyorkfed.org/research/staff_reports/sr957

Christoffersen, P. F. (1998). “Evaluating Interval Forecasts.” International Economic Review 39(4), 841–862. https://ideas.repec.org/a/ier/iecrev/v39y1998i4p841-62.html

Danielsson, J., & Shin, H. S. (2003). “Endogenous Risk.” In P. Field (ed.), Modern Risk Management: A History. London: Risk Books. https://www.riskresearch.org/files/DanielssonShin2002.pdf

Gilchrist, S., & Zakrajšek, E. (2012). “Credit Spreads and Business Cycle Fluctuations.” American Economic Review 102(4), 1692–1720. Excess bond premium series and documentation: https://www.federalreserve.gov/econres/notes/feds-notes/updating-the-recession-risk-and-the-excess-bond-premium-20161006.html

Institute of International Finance (2026). Global Debt Monitor, Q4 2025. https://www.iif.com/Products/Global-Debt-Monitor

Minsky, H. P. (1992). “The Financial Instability Hypothesis.” Levy Economics Institute, Working Paper No. 74. https://www.levyinstitute.org/publications/the-financial-instability-hypothesis/